1. We have an arrangement with Bridgewater Associates that enable us, from time to time, to republish excerpts from Daily Observations, their weekday email to clients. With COP28 much in the news, we found yesterday’s brief — ‘Gaps in Financing Highlight the Challenges Facing the Net Zero Transition’ — particularly interesting and important. It addresses the obvious question: How much will the ‘Net Zero Transition’ cost and who pays?

What follows is a verbatim excerpt from the introduction to the full report. We are not able to allow you access to the full report.

How the net zero transition plays out—and the speed at which it occurs—will have major implications for corporate capex, commodities, and economies and markets more broadly. One lens into how this transition is unfolding is the state of bank-to-corporate green financing, which is not happening at a rate consistent with global net zero goals.

In previous Observations, we have looked at how global emissions are distributed across sectors, the role that investors and governments play in reducing them, and how an accelerated transition may affect investor portfolios. In this Observations, we turn our attention to another important piece of the puzzle—how the climate transition will be financed. Reaching net zero by 2050, to which countries collectively contributing 88% of global emissions have committed, will require a rapid scaling up of renewable energy, as well as the phasing out of the dirtiest sources of energy, such as coal. In addition, industrial processes will need to be overhauled massively, and new technologies such as carbon capture will need to be developed. Seeing what activities are being financed can be a window into questions such as how the capex cycle is playing out across sectors and geographies, how climate policy is flowing through to actual investment, and how commodity demand and the energy mix are likely to shift in the years ahead.

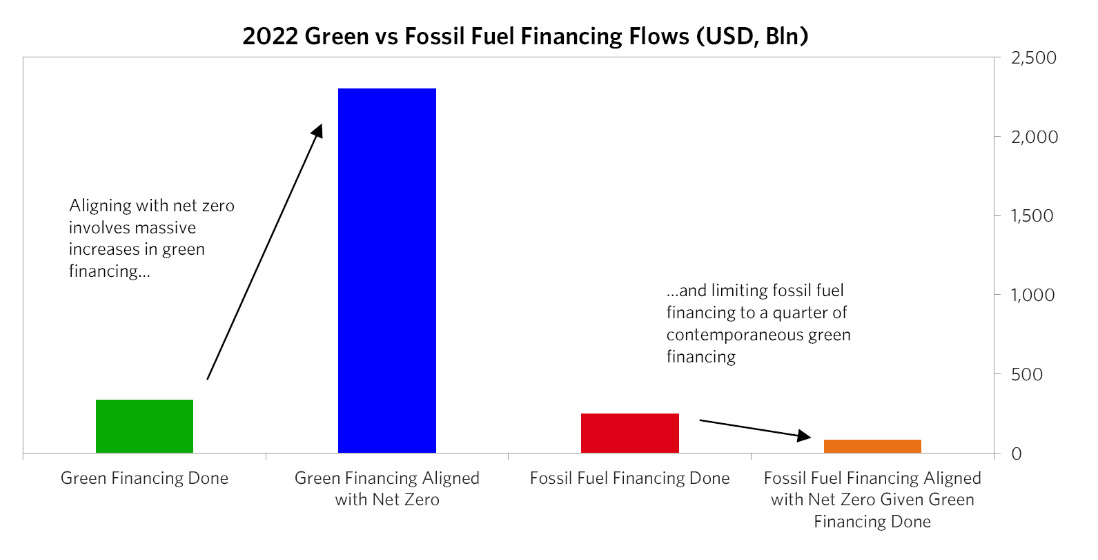

To align with global net zero goals, the world will require massive investments in low-carbon technologies. Estimates from the Glasgow Financial Alliance for Net Zero and McKinsey point to at least $125 trillion of cumulative spending from now to 2050, with around $30-55 trillion of this coming within the next decade. On an annual basis, this amounts to ~$6 trillion from a variety of public and private sector players, such as governments, banks, and households. Banks are expected to make up a large share of this, at ~$2 trillion annually across lending and underwriting. As a result, bank-to-corporate green financing flows are an important lens into how the global climate transition is unfolding, and they give us insight into financing channels that are economically and technologically viable today (compared to areas of the transition that are still earlier in their maturity). While these estimates are not meant to be precise, they convey the scale of the capital investment required to finance the climate transition.

When we analyze thousands of individual loans and debt/equity underwriting activities from the 200 largest global banks, we have seen a surge in bank-to-corporate green financing flows over the last few years (more than double since 2018). But on the whole, these flows are not happening at a rate that is consistent with global net zero goals. Of the ~$2 trillion of annual bank-to-corporate green financing flows that we reference above, less than a quarter, or ~$400 billion, occurred in 2022, due to factors such as limited (but growing) demand for green credit from corporates and uncertainties around government policy and the profitability of emerging climate technologies. And while the absolute level of “brown” financing to fossil fuels has been stable over the last few years, the corresponding demand for green financing has not risen quickly enough to reach the 4:1 green-to-brown energy supply financing ratio that BloombergNEF estimates to be compatible with net zero. Looking ahead, concerted action from multiple players (e.g., governments, companies), as well as the continued development and commercialization of new climate technologies, will be needed to meaningfully shift the world’s energy infrastructure and support the net zero transition.

— Karen Karniol-Tambour | Daniel Hochman | Jeremy Ng | Alexis Teh (Source: Daily Observations, with the expressed permission of Bridgewater Associates)

2. Why is everyone so gloomy? Political News Items’ answer to every question about the current public mood is: ‘things are out of control.” David Wallace-Wells, whose work is always worth reading, is a bit more….specific:

The outsize effect of inflation has been the most commonly offered hypothesis in debates over the “vibe-cession”: While the inflation rate has slowed considerably, prices are stable only at much higher levels than even three years ago. Other theories: that partisanship is clouding our judgment, that the media is shoving too much bad news down our throats, and that the grimmest takes invariably take over TikTok. There are other propositions, too, each weedsier than the next: that wage gains powered by pandemic relief were reversed when that stimulus was withdrawn, that rent and the cost of homeownership are driving generational despair, and so on.

But in fishing for causes, an obvious contributor is often overlooked: the pandemic itself. It not only killed more than a million Americans but also threw much of daily life and economic activity and public confidence into profound disarray for several years, scarring a lot of people and their perceptions of the country, its capacities and its future.

When Americans are asked whether the country is on the right track, or whether they themselves are optimistic or pessimistic, they don’t treat the query like a trivia quiz about the last quarter’s G.D.P. growth or the Black unemployment rate or even the size of their own paychecks or stock portfolios. They are effectively responding to the therapist’s query: How are things? They answered that question according to one set of patterns, stretching back decades. And the pattern did not begin to shift only when inflation peaked in late spring 2022, or when pandemic relief was relaxed in fall 2021, or when supply-chain issues first arose earlier that year. They began answering differently in 2020, as the scale and duration of the pandemic came into view.

For decades, surveys about the economy were an accurate gauge of economic fundamentals that, practically speaking, there was little need to distinguish between the two.

That all changed in early 2020, when a significant gap opened between economic conditions and public perception. Perhaps the most vivid illustration of this gap comes from The Economist, which trained a computer model to use fundamental economic indicators to estimate consumer sentiment. Using those indicators, the model was able to quite closely predict public sentiment, showing a very close correlation between economic fundamentals and public perceptions that stretched back at least to 1980.

Then, in early 2020, the correlation evaporated in the United States. At first, the fundamentals tanked while Americans maintained a rosier view of things, but this relative optimism was pretty short-lived. By the fall, the gap had opened up in the opposite direction, with Americans more pessimistic about the economy than the “fundamentals” model predicted. By the spring of 2021, the gap was about 20 points. By the end of the year, which was both the deadliest in the pandemic and when inflation first arrived, public confidence was 30 points lower than the model suggested. By June 2022, when inflation peaked just after the cessation of the Omicron wave, the gap was about 35 points. (Source: nytimes.com)

3. By now we all know that Argentina’s new president, Javier (“El Loco”) Milei, is a right-wing lunatic, politically inept, in way over his head. His presidency, it’s said with certainty, has a rendezvous with failure, sooner rather than later. How could anyone imagine any other outcome?

Gas from shale fracking will soon be flowing abundantly through a new pipeline from Vaca Muerta, a region of northern Patagonia containing the world’s second largest reserves of shale gas and enough oil to produce a million barrels a day by 2030 at a break-even cost of $35-40.

Argentina will no longer have to bleed its dollar reserves to import liquified natural gas. It will be earning energy dollars.

Argentina holds 21 percent of the world’s proven lithium reserves. It is today producing just 6 percent of supply. This is about to change.

Thirty lithium projects are being developed in the Andean uplands of Catamarca, Salta, and Jujuy, many in joint-ventures with the Chinese. The area is among the planet’s most lucrative deposits, extracted cheaply from brines on sun-drenched salt plains using solar power, with a carbon footprint seven times lower than Australian spodumene.

Lithium prices have crashed by 75 percent but this cannot last. There is a structural shortage of the EV battery metal, which is why Elon Musk is so assiduously courting his fellow libertarian in Buenos Aires.

Argentina’s mining ministry says production will rise by 50 percent this year alone. Eurasia Group expects output to increase tenfold by 2027.

Milei enjoys goading the eco-literati on global warming – a “socialist lie” – but he will not let it stand in the way of an EV lithium boom. He has picked an enthusiast to be the new mining chief. The industry is purring with delight.

Argentina is the world’s biggest exporter of soybeans, and a major force in wheat and maize. La Niña and the worst drought in living memory cut grain output by 45 percent last season, depriving the country of $20 billion of export earnings. This bad luck was the straw, setting off the final run on the peso.

The return of El Niño is bringing back the rains, and refilling the hydro power basins. Grain dollars will soon be arriving again…….

There is a near-consensual view in the posh global media that Milei is a borderline nutcase and that his plans are absurd. I would suggest that he may instead succeed, setting off a wave of Hayekian ferment and helping to bury the “dependency theory” doctrines of Raul Prebisch, which have so blighted economic thinking across Latin America.

To the extent that he resists the current infatuation in the Global South with China’s Leninist economic model, all the better. We need Argentina back in the West, where it belongs. (Source: telegraph.co.uk)

4. Germany.

The populist right-wing Alternative for Germany (AfD) party has gained a significant lead over its rivals in the east of the country, where it is now polling at more than 30 per cent of the vote in every state except Berlin.

While the party has long regarded the former territory of the communist East Germany as its electoral heartlands, surveys suggest it is increasingly establishing itself as the strongest political force across the region.

The mainstream parties are concerned that the AfD, which has yet to win an election at state level, may score a series of thumping victories in the east next year.

This in turn raises the prospect that the centre-right Christian Democratic Union (CDU) could strike some form of bargain with the AfD, breaking one of the central taboos of modern German politics.

The two parties are already working together on several district councils and in some recent cases have tacitly joined forces to push through legislation in east German state parliaments.

At a national level the AfD is consistently polling at about 22 per cent, riding a resurgence of public concern about immigration and the health of the economy.

Why it matters: Trump would fill the most powerful jobs in government with men like Stephen Miller, Sen. J.D. Vance of Ohio and Kash Patel — with the possible return of Steve Bannon. If Trump won in 2024, he'd turn to loyalists who share his zeal to punish critics, purge non-believers, and take controversial legal and military action, the sources tell us.

Trump and his prospective top officialsdon't mince words about their plans:

What's happening: Trump hasn't settled on specific roles for specific figures, and hates it when his staff and friends speculate otherwise. It's not in his DNA to do detailed personnel planning, and a lot depends on the last few people he's talked to.

But in rolling conversations with friends and advisers, he's been clear about the type of men — and they're almost all older, white men — he'd want to serve at his pleasure if he were to win a second term.

Between the lines: We wrote last month about the multimillion-dollar effort to vet loyalists for up to 50,000 lower-level government jobs in a Trump administration. This is about their potential bosses.

It's unclear who would land where, but make no mistake: These are specific prototypes of Trump Republicans who would run his government. This is very different from the early days of his first term, when he was restrained by more conventional officials, from John Kelly to James Mattis to Gary Cohn.

If Trump wins Iowa and New Hampshire by “comfortable” margins (which means double-digit margins), then he’s the 2024 GOP presidential nominee. It’s as simple as that.

The rough math of Iowa and New Hampshire voters is 40-45% are Trump-and-only-Trump, 30% are not-Trump and 25% are “Trump was a good president but maybe we should shop around, go in a different direction.”

Trump and Team Trump don’t care about the 30%. They’re hopeless. Trump and Team Trump keep a close watch on the 40%-45% bloc, in case they start getting ideas about going shopping. Trump and Team Trump have the opportunity to close the deal by appealing to the 25% who think Trump was a good president but are still shopping.

At his rallies, Trump is explicit in his “messaging” to the 25%. He constantly exaggerates how great things were when he was president and how awful things are now. The obvious message to the 25 percenters is: I’ll be a good president again, so don’t worry about all this other stuff. Stay focused.

That’s smart. That’s exactly what he should be doing.

But he hasn’t closed the deal with the 25% and one of the things that keeps them shopping is…Trump anxiety. He makes them nervous. At times he’s so crazy it doesn’t seem like he’s acting that way, it seems like he is that way. And so they continue shopping.

The Axios story quoted above was posted on Axios because the Trump campaign wanted it posted on Axios, because everyone who’s anyone in politics reads Axios, every day. And they then push it out on social media and by the end of the day everyone involved in politics across the country has read the story.

But what a weird message, right? If what seals the deal for you is some support from the 25 percenters, why would you plant a story that makes it more likely they will keep shopping? It doesn’t make sense. And whatever else you might think of the Trump campaign, its management (almost always) does things that make sense.

So why?

My guess is that the Trump campaign has a turnout problem amongst its core supporters in Iowa. Possible reasons for the problem include: overconfidence (Trump is going to win and therefore no need to show up for one’s local caucus), some attrition amongst evangelical voters, distrust of/paranoia about the process (GOP officials/strangers writing down names, addresses, phone numbers, etc. at the caucus locations) and lack of urgency (which is sort of the same as over-confidence).

In New Hampshire, some of the same problems apply, but a bigger one looms: cross-over voting. Independents and Democrats (if they’re willing to switch party affiliation on election day) can vote in the New Hampshire GOP primary. Since there’s no real point in voting in the now-unofficial Democratic primary, there’s a possibility the GOP primary electorate will swell with non-Republican voters, most of whom, presumably, dislike Trump.

What do you do when you need your base to show up? In the immortal words of former Alabama Gov. George Wallace, you “get it down there where the dogs can eat it.”

A not insignificant slice of Trump’s core support is responsive to authoritarian messaging, as the Trump campaign well knows. The fact that Team Trump is deploying that kind of messaging — on Axios for insiders (and the internet) and Sean Hannity’s television program for “the base” — at this stage of the campaign means that something in their poll data is amiss. If everything was fine, they’d be talking to the 25 percenters about the extraordinary, amazing, incredible success of Trump’s presidency.

Political News Items is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

The crossover vote in New Hampshire will help Nikki Haley overperform. Independents and Democrats are anti-Trump and see DeSantis as "competent Trump" so they'll vote for Haley.

But Haley will never be the GOP nominee. She is only to split anti-Trump vote allowing Trump to win.

The crossover vote in New Hampshire will help Nikki Haley overperform. Independents and Democrats are anti-Trump and see DeSantis as "competent Trump" so they'll vote for Haley.

But Haley will never be the GOP nominee. She is only to split anti-Trump vote allowing Trump to win.